|

|

|

|

|

|

|

|

|

|

New Year. New Opportunity!

What opportunities will you have to buy or sell a home this year? Don’t think you’ll have one? Think again!

Let’s start by looking waayyy back to December 2023, and then we’ll look forward. Aside from the seasonal slowdown, higher interest rates and low inventory, have had the most impact on the market. You can dive deeper by clicking the full Denver Real Estate Market Trends report, and know I’m always here for you with home values and neighborhood trends catered to your specific needs. Now, back to the future.

In my experience…

Winter is the best time to buy a home. Fewer buyers are willing to face the cold, postponing their shopping for early spring, giving you an opportunity to make an offer with less (or no) competition. And sellers who sell in the winter generally have good reason to. This means their motivation is driven by their needs rather than their wants. Another opportunity!

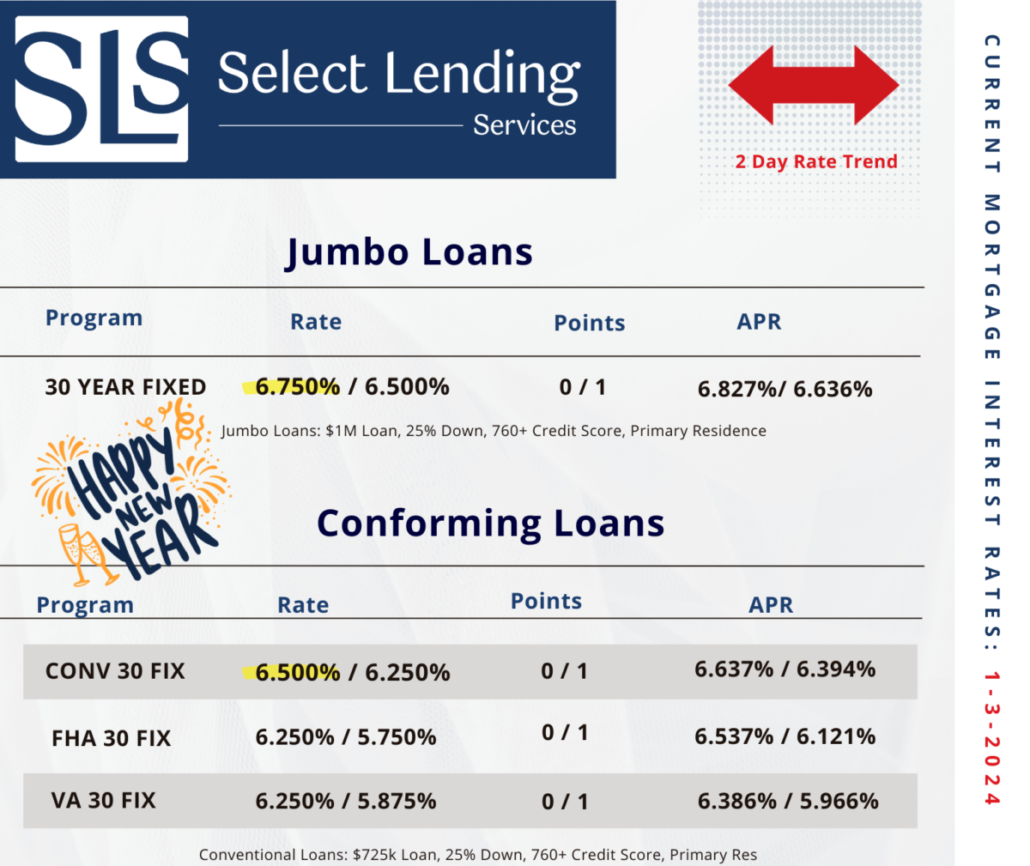

Waiting for the rates to fall? Don’t. While nobody knows for sure what will happen in 2024, we are anticipating multiple rate drops as the economy stabilizes, but the “waiters” often lose. Think about it. If you buy early, you’ll be gaining equity as prices rise with demand. Buyers who wait to time the market will face a different set of challenges. Lower rates bring more buyers, bidding wars and higher prices which increase the gains for those willing to buy now and refinance once all that rate dropping happens. Today’s rates from my lending partner, Select Lending Services, look a lot better overall than where we were last year.

Let’s talk about how 2024 can open a real estate opportunity for you!

|

|

|

|

As a Realtor, out on the town I’m always asked, “How’s the market?” It’s the follow-up question where it really gets interesting.

As a Realtor, out on the town I’m always asked, “How’s the market?” It’s the follow-up question where it really gets interesting.

The last seven years have seen a surge in the metro Denver real estate market as record numbers of buyers look for homes, which in turn has caused prices to jump. The strength in the market has been so pronounced that people are beginning to ask “Are we in another bubble?” It’s a reasonable question given the horrendous experience of the housing crisis, and while no one can ever predict the future with certainty, I see no evidence that we’re heading for a dramatic downturn in the real estate market any time soon. Here’s why:

1. Even with the continued increase in metro Denver home prices (up another 8 percent in the past 12 months) the average inflation adjusted PITI (Principle, Interest, Taxes, and Insurance) payment made in metro Denver is actually BELOW our 35-year average. This means that while prices have steadily risen, buyers are still able to afford their monthly payments, providing plenty of room for continued home price increases.

2. The number of transactions relative to the population of metro Denver is just about at the 25-year average. At the peak of the bubble in 2006 the number of home sales was about 20 percent above the historical average. When we see the number of closed transactions well above our historical average that’s an indication of an overheated market, as it was in 2006. The number of closed home sales is actually DOWN 12 percent in the past year due to the low inventory. No sign of a bubble here.

3. In 2006, many of the deals were closed with low or no documentation mortgages (“liar loans” or “no doc loans”). Today, mortgage underwriting standards are among the toughest they’ve been in decades. This prevents unqualified buyers from purchasing property, which mitigates the chance of the market overheating (fewer buyers means fewer purchases means less chance of the market frothing into bubble territory like it did in the past).

4. Because of relatively high home affordability it’s a lot cheaper to buy than rent in our market. This would not be true in a bubble. For housing price affordability to return to the average level that we saw in the years between 2000 and 2004 either home prices would have to increase an additional 35 percent or interest rates rise to 6.6 percent. Neither is going to happen any time soon.

5. The imbalance between buyers and sellers we’ve seen recently in our housing market (too many buyers/not enough homes for sale) is due to a lack of inventory, not illogical/unrealistic/unsustainable demand from buyers. “Much of the price increases we are seeing are the result of rising demand among investors and homebuyers for a still-limited supply of homes for sale,” said Anand Nallathambi, president and CEO of CoreLogic. This imbalance is a logical correction from years past when we had too FEW buyers in the market. This is how markets are supposed to work, always regressing to the mean over time.

6. Rising mortgage rates will help to temper the possibility of a bubble as well (they are still near 50-year lows but are expected to rise someday). “History shows that a rapid rise in interest rates tends to have little correlation with home prices. Rather, rising rates are more likely to contribute to a decrease in home purchase volume,” wrote Mark Palim in a Fannie Mae commentary. So the positive side of a rise in mortgage rates is that it will reduce the number of buyers and therefore lower the chance the market will rise out of control and end up collapsing in a bubble.

Click on the monthly market snapshot, the inventory of metro Denver homes for sale continues to fall; it’s down another 5 percent from a year ago. Since the inventory is still extremely low (about 5,520 homes on the market where about 18,000 is a balanced market) I am all but certain the demand will still exceed the supply for the next several years and prices will continue to rise for the foreseeable future. No bubble on the horizon yet… Stay tuned!

![June 16 - Market Snapshot [5608]](https://tracyshaffer.com/wp-content/uploads/2016/06/June-16-Market-Snapshot-5608.jpg)

Buyers

If you agree that we’re not headed for a bubble any time soon what does this mean for you as a buyer? I think it means you should consider buying a home IF it makes sense for you to do so. Are you running out of room at home? Expecting a baby? Have an awful commute? Want to live in a nicer neighborhood? Looking for a better school district for the kids? There are a lot of great reasons to move. But don’t buy a home to speculate on the market; buy because it’s time for a new home. Call me anytime to discuss what your options are and how I can help you find a wonderful place to live.

Sellers

We have been discussing the incredible strength in our housing market. If you’re looking to sell your home this should be very welcoming news! The inventory of homes on the market is at an all-time low and prices are up. Call me and I’ll be happy to run a complimentary Comparative Market Analysis on your home to let you know what it might be worth. It’s great information and costs you nothing.

Investors

The most recent “Metro Denver Area Residential Rent and Vacancy Survey” shows the great news continues for landlords. According to the report:

“The overall vacancy rate for the metro area for the fourth quarter of 2015 was 3.1 compared to 3.9 percent for the previous quarter, and 1.5 percent for the fourth quarter of 2014. It was 2.0 percent in the fourth quarter of 2013, 1.7 percent for the fourth quarter of 2012, 2.1 percent for the fourth quarter of 2011, 2.0 for the fourth quarter of 2010, 5.5 for the fourth quarter of 2009, and 4.9 percent for the fourth quarter of 2008.”

In the U.S., more millionaires owe their wealth to real estate investments than any other single source of income. Today’s market could not be better for long-term buy –and-hold investors. Call me to find out more.

Vacancy Rates

Adams 3.9%

Arapahoe 4.0%

Boulder/Broomfield 2.7%

Denver 3.1%

Douglas 1.7%

Jefferson 2.6%

Let’s talk about homeownership. Are you considering buying vs. renting?

Renters often ask me if it’s too late to buy a house: Are we heading for a big downturn? Are we too deep in the market cycle to buy? they wonder. Timing the real estate market perfectly is extremely difficult, perhaps impossible, and some of these potential buyers were the same renters that were sitting on the fence when the market was down, even once we’d passed the nadir. I believe that buying a home is less about the market and more about life; your life. So don’t try to time the market, take a look at your life, the low interest rates and time that!

1.) Are you getting married, starting a family, or tired of paying skyrocketing rent without having an asset to show for it? Would you like to have more space; a backyard for the dog, the kids, the BBQs, or the tomatoes? Do you like the idea of being part of a neighborhood, community? Perhaps you got a nice raise, job or promotion and you’d like to set down roots, do you plan on staying in one place for at least five years? Do you like the idea of investing in something that will build long-term wealth?

These are the types of questions you should be asking when you are considering homeownership.

Here’s another thing to keep in mind. In the U.S., the average total net worth of rental households is $5,800. Compare that with the average net worth of a home-owning household at $199,500 and you’ve got worth 34 times more than those who rent! There’s no doubt that over the long term, homeownership is a solid way to build wealth and financial security. I often advise my first-time buyers to get into something affordable now (not so easy in Denver these days, but doable) and then move up when life allows. If you can keep that first property as a rental, it’s a great way to invest in your financial future.

2. Interest rates remain at record lows but this can’t last forever. No one knows when they’re going to rise, but news this week gave hints of a rise as early as June. Though home prices have gone up the past several years, low interest rates continue to make homes relatively affordable— especially compared to renting. Once interest rates rise, the door to home affordability will begin to close for a lot of potential buyers, leaving them sorry they didn’t act when interest rates were at 50-year lows.

Let me break down the numbers. Assume you are purchasing a $210,000 condo with a 5 percent down payment. The Principle + Interest payment at 4% interest would be $952 per month (tax and insurance and HOA not included). An interest rate increase of one percent (5%) would take your payment of $1,070 per month—an increase of $1,416 a year. Now assume that rates tick up to 6 percent. That increase would result in a 21 percent increase in payments from $952 to $1,196. Where you really see the effect of these increases is when you hold the property for the full 30 years. On a $210,000, 30-year fixed-rate mortgage that increases from 4 to 5 percent, the borrower who obtains the 5 percent loan would pay an additional $42,772 in extra interest as opposed to the borrower who paid just 4 percent interest. Though most buyers consider their monthly payment as most important, when you look at the life of the loan you’re paying a lot more in the total loan amount. This is a great reason to make a “move-up” move right now. Say you’ve outgrown your place, it may be time to cash out and get your “forever home”, or like I mentioned, use your current home as an income property and let your renters pay off your mortgage.

The main reason the average home owner has so much more personal wealth than the average renter is that homes appreciate in value. Over the past 45 years, homes in metro Denver appreciated 6.3 percent per year. If you buy a $200,000 home, you can expect over the long term its value to rise about 6 percent every year. This means you’d make $12,000 in appreciation the first year, an additional $12,720 the second year, another $13,483 in the third year, and on and on. Contrary to popular belief, only 4 of the past 45 years did prices actually fall in metro Denver.

If you’re still wondering whether you’d be better off renting or buying, Trulia built a great Rent-vs-Buy tool. Answer a few simple questions and the system tells you whether it makes more financial sense over the next seven years to rent or purchase. I think it’s worth a couple minutes of your time to see what you can learn – you’ll really like it!

Key Messages for May

Prices are up 8% in the prior 12 months vs historical 6%. Inventories are tighter than last year, especially for small, lower priced homes. In 2016, we expect 8-9% appreciation, flat unit sales volume increases, and continued tight inventories.

Everybody loves Zillow. I love Zillow. I love how excited it gets buyers and sellers when they see a home they love or what a neighbor’s house is selling for; a useful tool in many ways, for better or worse, it empowers the consumer. I look at Zillow to see what my clients/potential clients are taking as accurate information… and then I do my homework. The #Denver #realestate market is moving so quickly that even agents and appraisers can have a hard time keeping up. Public record algorithms don’t have the ability to distinguish the differences in the quality of one property from the other, upgrades, location, or if there’s a crack house next door. Algorithms don’t call other agents to inquire about that “Coming Soon” sign or have the latest data on solds as it takes some time to record.

The Los Angeles Times recently published an article that lays it out quite clearly. Though a “Zestimate” can have a low margin of error, it can also be alarmingly high. Imagine a scenario where you’re meeting with your perspective agent thinking that your home is worth 26% more than what it will really sell for.

Sellers, armed with the Internet, often have an idea in their heads about their home’s value. When I pull comparable properties, show them what the list vs sold prices are and how many days on market it’s taken those homes to sell, they may find a different story. Sometimes the news is good, based upon my data, their home may be worth more than they think. Other times it can be a let down.

Buyers burn the midnight oil searching Zillow then send me a link to their dream home. When I hit the MLS at 7 a.m. most often I find that this dream home is under contract… or sold three months ago. If you’re looking to buy a home, I’ll send you to REColorado, the consumer website linked to the Denver Matrix MLS I use so we can work together efficiently. It’s updated throughout the day, has great home search capabilities and saves me time looking for your real home, not the one someone’s already moving in to.

All this to point out that you now have access to a lot of information about my business. A lot of it is helpful and a whole lot of fun, but none is as accurate as hiring a professional; one who specializes in finding the right home in the right neighborhood that suits your needs. If you’d like an “Exact-i-mate” about what your home might sell for in today’s Denver market, give me a call I’d be glad to sit down with you and show you your market value and why.

As the clock ticks toward year’s end, it’s time to review the 2015 real estate market.

As the clock ticks toward year’s end, it’s time to review the 2015 real estate market.

When someone asks me how the real estate market is, the cocktail party answer is that it’s been a very pleasing 12 months and future looks bright and shiny. Because the economic news is good our Denver Metro real estate market is projected to stay strong but not overheat. I’ll share some of the metrics I use to evaluate the market and understand it better, describing what 2015 looked like and where I think we’re headed.

Market strength–2015 was an extremely strong seller’s market. The market strength peaked in the spring when the bottom dropped out of our inventory and multiple offers were all the rage. Frustrating for buyers who felt they had to give away so much to stay competitive, the good news is that the market reacted appropriately and became more balanced as the year progressed. With prices on the rise, sellers were motivated to sell as we approached the fall so the market cooled with the start of school and the weather. It is still a strong seller’s market, but far more in balance. I expect 2016 to continue along this line and see no sign of a major imbalance that could lead to any sort of ugly peak and crash. Sellers should get a good price for their homes and replacement properties should not be as hard to find.

Buyers– Real estate website Trulia says that buying an average home in Denver is a whopping 38 percent cheaper than renting a home! For the average home, the interest rate would have to skyrocket to 11 percent for renting to become cheaper than buying, meaning that it is currently MUCH more affordable to buy than to rent. Even with current prices and current rents, interest rates would have to nearly triple to make renting more affordable than owning. (Call me if you want to talk about this.)

Sellers-Can’t say this enough: the most important thing to prepare your home for sale is to get rid of clutter. This includes furniture. You may have learned to live with that cherished armchair stuffed into the corner but a professional stager will often times whisk away half of your furniture. The house looks so much bigger for it, leaving space for a buyer couple and their agent to tour the home without bumping into each other, and space for their imaginations to make it their own. You don’t have to go “Stager drastic” but take a hard look, be objective, and see what you can live without. Painting always pays for itself and statistics show that springing for a staging company is often a good investment.

Rental Vacancies– The rental market is stronger than it has ever been in metro Denver. The vacancy rate for 1- to 4-unit properties is an extremely low 2 percent. That’s a drop from the already 4.7% we’d been experiencing for the past few years. On top of this, rents are rising faster than ever, up 30% in the past three years. With rents equaling a mortgage payment, we’re seeing more renters making the decision to buy. Why live waiting for another rent increase, tough competition and another application process without building any equity? Many homeowners who lost their homes in the downturn and have been renting, are becoming eligible to purchase once again. This is great news for the market and will certainly lead to more sales in 2016, though the influx of buyers insures a continuing seller’s market.

Interest rates– No one knows exactly what interest rates will do in the future but my best guess is that they may rise a little in 2016, but only a little. Remember that the Federal Reserve has control over only short-term, not long-term interest rates. Even if the Fed raises rates, that doesn’t directly affect the 30-year home buyer interest rate you are concerned with. Long-term interest rates are affected by the bond market (as bond prices decrease, interest rates increase) which, frankly, is not predictable. Understand though that interest rates are at near 50-year lows so they are highly unlikely to fall any further. All we know for sure is that someday they will go up.

The Economy– No matter what you may hear in the months leading up to the election (places hands over ears), right now the metro Denver economy is very strong. This is fueling our terrific real estate market and the rising population of our city. The unemployment rate is extremely low, about 3.5 percent. Inflation will stay in the range of 1-2 percent, our population is rising at a rate of 50,000 people/year and consumer confidence continues to rise. Nothing can be better for the housing market than a strong and steady economy.

Mortgage -The single most important number for a home buyer is their FICO score. For good or bad, your FICO plays a major role in your ability to finance your home purchase. Your credit score is a snapshot taken by the three leading credit bureaus, TransUnion, Equifax and Experian, to help lenders determine what sort of credit risk you are. Your FICO is a number between 300 and 850 and is calculated by a complex algorithm assessing your past credit history. Most home lenders will consider a score over 700 to be excellent while scores below 600 are considered poor. The better the score the more credit will be extended, at better terms, with a lower interest rate. The best credit terms are extended to consumers with scores above 740. Therefore, it’s critical to understand what your FICO is and what you can do to improve your score. When I work with buyers I help them understand the factors affecting their score so they can work to improve them. I can’t think of a better investment in your future than to spend a little time working on your FICO score.

Here are a few tips I give my clients:

1.Don’t max out your cards, try to keep them under 50% of available credit. Running high balances can severely impact your FICO.

2.Continue paying your bills on time.

3.Don’t apply for new credit or cancel an old card because length of credit helps.

4.Pay down high balances.

5.Dispute and resolve any inaccurate items in your credit report.

6.Invest in a credit monitoring company to track the changes to your score.

I’m frequently asked where the real estate market is headed and when we will get back to some kind of equilibrium. The truth is it’s extremely difficult to accurately predict the future but here’s what I know: Right now we are experiencing one of the strongest seller’s markets in our history and we’re a full six and a half years into this market recovery. The reason is simple: we have much more demand for homes (buyers) than we have supply of homes (sellers). What’s fascinating to watch is the dynamic build on itself. It looks something like this:

I’m frequently asked where the real estate market is headed and when we will get back to some kind of equilibrium. The truth is it’s extremely difficult to accurately predict the future but here’s what I know: Right now we are experiencing one of the strongest seller’s markets in our history and we’re a full six and a half years into this market recovery. The reason is simple: we have much more demand for homes (buyers) than we have supply of homes (sellers). What’s fascinating to watch is the dynamic build on itself. It looks something like this:

1.Buyers make offers on homes and continue to lose out to higher offers.

2.Buyers get increasingly frustrated and begin to get more aggressive with their offers.

3.The momentum builds on itself until we see what is occurring today, with multiple offers on a propertythe norm rather than the exception.

4.The multiple offer dynamic almost always bids prices higher than the original asking price.

5.The buyers that lose the bid learn from the experience and become more aggressive on their next offer.

6.Then back to Step 1, until the buyer bids high enough on a property to finally get an offer accepted.

The result of course is the tremendously strong seller’s market we have experienced for the past several years. And this seller’s market is not going to change any time soon, at least not until we get back to some kind of balance in the market between buyers and sellers. I don’t see that happening for at least several more years. In the meantime, if you’ve thought about selling your home, now might be a great time to find out what the market is like in your neighborhood and see what your home is worth. It’s almost certainly worth more than it was just a few years ago. Drop me a line and I’ll put together a professional Competitive Market Analysis on your home so you have the data to make the right decision.

Another question my potential sellers often ask is if they sell today, can they find a replacement home in time to move? In a market like ours this is a very good question. Fortunately, there are a number of things savvy sellers can do to take advantage of the seller’s market and put themselves in a good position when looking for their replacement home.

Here are a few:

1.First and foremost, work with an experienced agent to write a strong, professional offer on the home you want to buy. In a dramatically competitive market like we have now, weak, poorly written, unprofessional, and bad offers just aren’t taken seriously. There is both an art and a science to writing a strong offer. Call me and I’ll explain more about how to write an offer that has a great chance of getting accepted.

2.Add a contingency clause to your contract to buy another home. The clause would say that you will close on the home you are purchasing once your own home sells. The problem with this is that it somewhat weakens your offer as many sellers don’t want to accept a contingency when they can sell quickly to the next buyer. But occasionally we do run across a seller that is in no hurry and is happy to wait for the buyer’s home to sell.

3.Lease the home you just sold from the buyer for a period of time while you are looking for your new home (this is called a lease back). Some buyers do not want or are not able to move into their new home immediately and this permits them to earn rent from you for the period of time you are shopping for your next purchase, a win-win situation. 4.Look into a new construction purchase. Builders are building as fast as they can in this market to keep up with demand and there may be inventory of completed or soon-to-be-completed homes that could suit you. 5.Arrange to stay with family or move into short-term rental housing until you find your next home. While not a perfect solution I believe it’s far better to inconvenience yourself for a short period of time than to settle for anything less than your dream home!

“Denver apartment rents rising three times the national average”

This was the Denver Business Journal’s Sept. 2 headline. Denver rents have increased another 7 percent in the past year, which is three times the national average of 2.3 percent. And given the continued lack of rental inventory, rents are expected to continue increasing at a strong pace. Sooooooo…. 1.If you’re a renter it might be time to consider looking into buying a home to get out of the rental market madness! 2.If you’ve ever thought about buying a rental as a long-term investment now might be the time to learn how to purchase a safe, cashflowing property. Interest rates are still near record lows and rents havenever been higher, a wonderful combination for any real estate investor.

Mortgage rates continue to hover at near-record lows. For homeowners looking to upgrade to a larger, better home, low rates combined with low home inventory are making this a great time to upgrade to a larger home with very nearly the same monthly payment. We have several recent examples of clients selling their current homes and getting into a $40,000 – $50,000 more expensive home with the exact same monthly payment. Please give me a call or send me and e-mail and I’ll do a free analysis to see if this might be a good scenario for you to take advantage of.

From Page 4

4. The Investor Real Estate Market: Denver is still a great place to invest in real estate. The fix and flip market is strong for those who can find underpriced homes to buy and repair. They’re out there but it takes tools, patience, and work to find them. Once you get one fixed up, selling is the easy part because of the lack of competing inventory. The buy and hold market will continue to be extremely profitable for long-term investors. Interest rates and vacancy rates are still near record lows and rents continue to rise – a record 10.8 percent per year the past three years. It’s not difficult to buy a rental property in today’s environment and put it on the path to be paid off in 12-15 years. Just think how your life would change if you owned a couple of rental properties free and clear! For building long-term wealth it’s tough to compete with rental property ownership. That’s the one thing that will never change. CLICK ON MAP TO ENLARGE

Need more info? Boy you are a real estate geek! (and I love it) CLICK LINK for the metrics from Matrix. 15-0705 DSF Data CITY – Copy

If you would like a personal real estate consultation, have any questions about the market, your home’s value or need more specific information about your neighborhood please give me a call.

Until next month… use your sunscreen!

Five Essential Things You Need To Know About the 2015 Summer Home Buying Market

This year has kicked off with an array of experts trumpeting the Denver housing market’s strength and resilience. Inventory is at record lows, home prices continue to rise, and foreclosure activity has ebbed to lows not seen since before the 2007 downturn. Spring and summer is the time for selling houses. The months of April, May, June, and July typically account for more than 40 percent of all housing transactions annually, thanks in large part to good weather.

1.Inventory shortages: “The story of the day is on the inventory front,” stresses Lawrence Yun, chief economist of the National Association of Realtors (NAR). It’s a sentiment echoed by many. The number of available homes in metro Denver has plunged to a record low, thanks to both an abnormally small supply of existing homes for sale and a dearth of new construction not keeping pace with the current demand.

2. Increased Competition: In addition to a dwindling supply of available homes, the number of buyers has surged. And not just traditional buyers – investors have comprised a sizeable chunk of the buyer pool since the downturn and continue to do so. Real estate investors are responsible for about 25 percent of the existing home sales each month. You, the prospective buyer, need to be prepared to move fast if you find a property you’d like to buy. “Buyers need to be patient because many will be outbid by others and might have to bid on multiple homes,” cautions Jed Kolko, chief economist of Trulia. Yes, indeed.

3.Cash is Still King: Given the steep competition, all-cash buyers who can close a deal relatively quickly offer great incentive to sellers. “Cash will still be king if there are multiple bids because from a seller’s view, they want a deal with fewer hiccups, “says Yun. My sellers are surprised to hear that about 30 percent of home sales each month are all-cash purchases.

4.The Good News: Lending Tree chief executive Doug Leboda says in light of the recently unveiled new home-lending standards, lenders are slowly starting to make it slightly easier to get approved. Talk to a couple of lenders, they’ll tell you things have improved over the past few years on the loan front.

5.More Good News: We are seeing a definite correction in the appraisal business. A few years ago appraisers were consistently under-valuing properties, reacting to the over-conservative nature of their shell-shocked underwriter patrons. Today we are seeing the vast majority of appraisals coming in at value, killing far fewer deals than in the past.

Buyers– If you’ve been considering buying a home it’s critical to understand the amazing tax benefits you’ll enjoy. Talk to your CPA to get professional advice, but here’s a brief look at some of the tax benefits of home ownership:

1.The Purchase. The IRS says that in most cases loan discount points and origination fees are tax deductible to the buyer, regardless of who pays them.

2.Mortgage Interest. In general, you can deduct interest charged on a loan used to acquire or improve your principal residence in the year that it is paid. In the early years of a loan, most of your monthly payment is interest, so this can really add up. If you are in a 28 percent federal tax bracket, this can have the effect of lowering your borrowing costs by almost a third.

3.The Sale. If you have owned and occupied your principal residence for at least two of the past five years, you can earn up to $500,000 on the sale of that house and pay no federal income tax whatsoever. That’s assuming you are married – singles get up to $250,000 tax free. You can do this as often as every two years for the rest of your life with no limit on the number of times you do it! The one restriction is that you MUST own and occupy the house as your principal residence.

Sellers– Month after month in this newsletter we have discussed the incredible strength in our housing market. If you’re looking to sell your home this should be very welcome news! The inventory of homes on the market is at an all-time low and prices continue to climb. Call me and I’ll be happy to run a complimentary Comparative Market Analysis on your home to let you know what it might be worth. It’s great information and costs you nothing.

Investors -For years our clients have been buying rental properties in metro Denver to build their long-term wealth. Our record low vacancy rate is a big driver of why rental property has performed so well. First, the lower the vacancy rate the higher the demand for the property. More demand means landlords can be more selective with prospective tenants and can also charge higher rents. Rents have skyrocketed the past few years because the vacancy rates have remained so low. One of the reasons vacancy rates are so low is that many people still cannot qualify for a loan. I don’t expect this to change in the foreseeable future. We’ve had a huge shakeout in the lending industry and lending guidelines are still much stricter than they were a few years ago. Until lending standards ease up more I expect vacancy rates to remain low and keep my investor clients happy. If you’ve ever thought of investing in a condo or house as a rental property call me and I can show you what the numbers look like and what options you might have. Graphic Mortgage The mortgage market continues to remain strong with historically low interest rates. Low rates combined with low home inventory are making this a great time to sell your home and move up to a larger home with the same or lower monthly payment. We have several recent examples of clients selling their current homes and purchasing new ones costing $40,000 – $50,000 more with the exact same monthly payment. Drop me a line and I’ll do a free analysis to see if this might be a good scenario for you to take advantage of!