|

|

|

|

|

|

|

|

|

|

New Year. New Opportunity!

What opportunities will you have to buy or sell a home this year? Don’t think you’ll have one? Think again!

Let’s start by looking waayyy back to December 2023, and then we’ll look forward. Aside from the seasonal slowdown, higher interest rates and low inventory, have had the most impact on the market. You can dive deeper by clicking the full Denver Real Estate Market Trends report, and know I’m always here for you with home values and neighborhood trends catered to your specific needs. Now, back to the future.

In my experience…

Winter is the best time to buy a home. Fewer buyers are willing to face the cold, postponing their shopping for early spring, giving you an opportunity to make an offer with less (or no) competition. And sellers who sell in the winter generally have good reason to. This means their motivation is driven by their needs rather than their wants. Another opportunity!

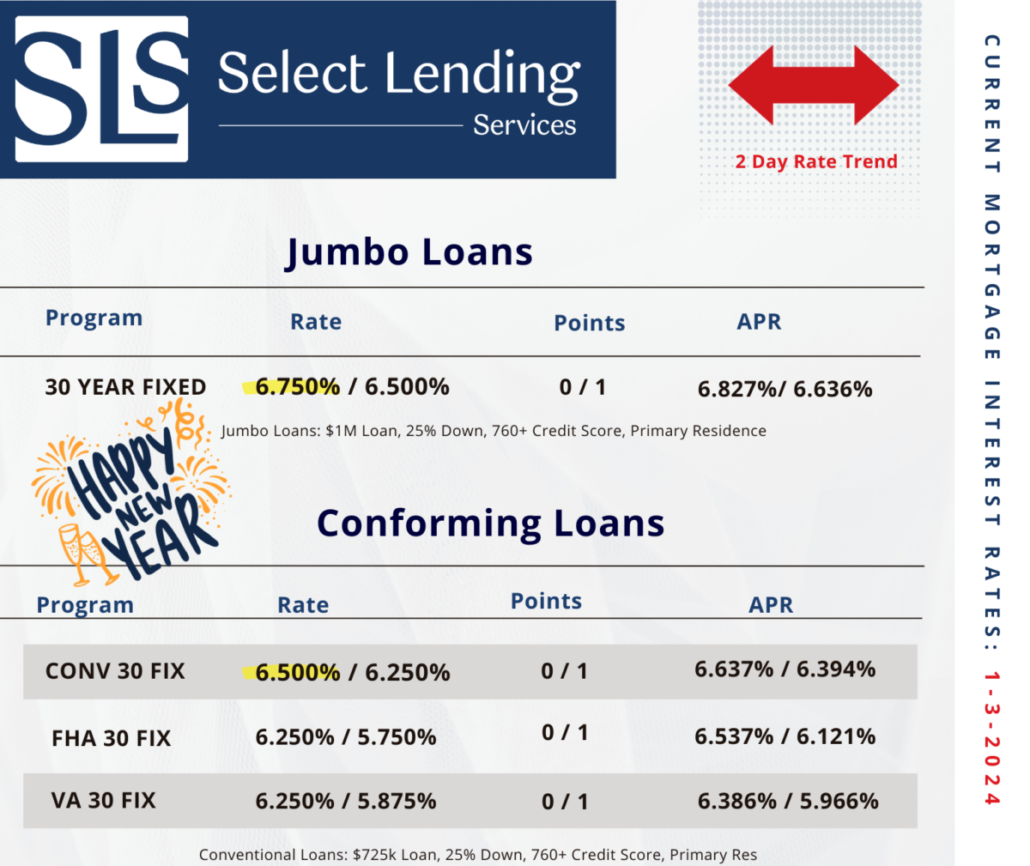

Waiting for the rates to fall? Don’t. While nobody knows for sure what will happen in 2024, we are anticipating multiple rate drops as the economy stabilizes, but the “waiters” often lose. Think about it. If you buy early, you’ll be gaining equity as prices rise with demand. Buyers who wait to time the market will face a different set of challenges. Lower rates bring more buyers, bidding wars and higher prices which increase the gains for those willing to buy now and refinance once all that rate dropping happens. Today’s rates from my lending partner, Select Lending Services, look a lot better overall than where we were last year.

Let’s talk about how 2024 can open a real estate opportunity for you!

How would it affect you if you could no longer write off the interest you pay on your mortgage?

According to panelists at Friday’s housing forum hosted by Zillow and the University of Southern California’s Lusk Center for Real Estate:

The burgeoning federal debt makes it unlikely that the mortgage interest tax deduction will survive in its present form. Of course, any proposed changes to the tax break for homeowners will spark a fierce debate over the fundamentals of the U.S. housing market, the value of home ownership, and consumer behavior.

“Fierce debate” he says? I’d call it a jobs-killer! But then again, I’m in real estate. Change is never easy, but when it hits our pocketbooks and the government, it really hits home. I advise my clients to educate themselves, talk to their tax professional and view the tax benefits icing on the cake. Knowing the long-term financial upside leaves them feeling good and more secure as they move forward with their biggest single purchase.

“I think it’s entirely likely that something big is going to happen (with the MID) starting next year with either administration,” said Jason Gold, director and senior fellow at the Washington, D.C.-based Progressive Policy Institute, an independent think tank.

A Congressional contingent advocates for the elimination of the mortgage interest deduction to help address the nation’s debt and budget deficit. Obviously things must be done to right the problem, but sticking it to a Middle Class whose beginning to feel the effects of a post-crisis housing market recovery seems a bit harsh. At the end of this year, a series of tax increases and spending cuts are scheduled to go into effect automatically unless Congress acts to prevent or alter them. Revamping the mortgage interest deduction is on the table as a way to head off that “fiscal cliff” scenario. (I wonder how many of those guys have a mortgage.)

Two years ago, a bipartisan deficit reduction commission recommended scaling back the mortgage interest deduction, which is currently capped at mortgages worth up to $1 million for both principal and second homes and home equity debt up to $100,000 and the deduction is only for taxpayers who itemize.

The Simpson-Bowles commission proposed turning the deduction into a 12 percent non-refundable tax credit available to all taxpayers, capping eligibility to mortgages worth up to $500,000, and eliminating the deduction on interest from second homes and home equity debt.

Though that seems more reasonable to me than the first idea, the National Association of Realtors has consistently defended the mortgage interest deduction in its current form.

Highly critical of the recommendation and claiming any changes to the MID could depreciate home prices by up to 15 percent, they are promising to “remain vigilant in opposing any plan that modifies or excludes the deductibility of mortgage interest.”

So… we’re back to whose going to pay down the debt? And how.

The MID is a “tax expenditure,” meaning its cost must either be made up through higher taxes elsewhere or by adding to the debt, and it costs the government about $90 billion a year. Richard Green, the director of the USC Lusk Center for Real Estate, told forum attendees that reforming the MID is necessary for fiscal sustainability. “We need to get revenue,” Green said. “You need to make a judgment about what’s better or worse for the economy. In my opinion, it’s better to do it with tax expenditures, rather than rates, though you may have to do both to get to where we need to be.”

Because mortgage interest rates are currently so low, he added, “This may be an opportunity to do less damage by reforming the mortgage interest deduction than at other times.”

(I wonder what cuts would make this guy feel the pinch.)

The mortgage interest deduction is particularly polarizing because of the disconnect between how people use it and how it is perceived. Green gave the example of Texas where most people do not itemize their taxes (only about 30% of taxpayers do) so they cannot take advantage of the MID. This line of thought perplexes me. So… if more Texans itemized their taxes it would make things fairer? or does he mean that if they actually knew they could they would, adding to the deficit? And haven’t Texans done enough of that? 😉

No matter how the chad falls in the next three weeks, watch for ongoing and loud debates over the Mortgage Interest Deduction. *covers ears*

Source: Inman News, Andrea V. Brambila, Monday October 15, 2012

It took Dr. Richard Alpert, Timothy Leary and countless hits of LSD to learn one simple truth: Be Here Now. So what can the psychologist-turned-spiritual guru, Baba Ram Dass, teach you about today’s Denver real estate market? BUY. HERE. NOW.

With nary a trace of mind-altering substance in sight, I can honestly tell you that the time to list your home for sale in the Denver metro area is NOW.

“How now” you say?

• Because EVERYONE else IS WAITING until spring.

• Because buyers ARE out looking.

• Because SHOWINGS ARE UP and inventory is down.

• Because all FOUR OFFERS I wrote in January created a BIDDING WAR.

Now, we all know war is not the answer but in real estate, a competitive market results in sellers driving their purchase price above their asking price. At this point (Jan/Feb, so I’m being here this quarter) the demand exceeds supply and buyers are flying out to snatch up well-priced properties like savvy shoppers after Christmas at Filene’s Basement. There is simply not enough out there. And I’m not just talking of the under-$200-first-time-buyer/investor end of the market. A home priced at or around $300k is likely to move well, despite the common seasonal perception, the Super Bowl or the weather. On Friday, as constant snow flurries were rapidly accumulating inches, agents were rushing out to show homes in order to present their offer s before the “Highest & Best” deadline. (I know this, I was one of them.) Today I submitted an offer for a buyer on a property, sight unseen. The home fit his criterion and he’d been beaten out three other times, so today we take no prisoners.

If you are sitting on the sidelines, waiting for the winter storm to pass before you list your house, remember… you could be pushing up daisies before the crocus pushes through the frosty ground. Now, I don’t mean that in the literal sense of the metaphor, but in the BE HERE NOW spirit.

If you’d like more information on the value of your house, trends in your neighborhood, or a yoga class near you, send me a vibe, a text or find me on Facebook. As the guru said…“We’re all just walking each other home.”

― Ram Dass

Creativity is the strongest force on earth; artists, visionaries and innovators lead us into the future. We’ve got some mad skills that actualize potential where others may only see what is possible. Be sure to click on the Thriving Artist Alliance page above and I’ve created a lovely video to inspire you. CLICK HERE TO WATCH

How do you get into the real estate investing game? One house at a time. Real estate investing, like the stock market, can be daunting for some, but the payoff is worth the learning curve. My client, Kevin, became a landlord in 2007 with the purchase of his first rental property, half of a duplex in the City Park neighborhood of Denver. With a $150,000 purchase price and some minor upgrades to suit his specifications, Kevin was able to create positive cash flow within a few months. Two years later, we looked for another property, scouring for a neighborhood where you could still find a bargain, yet prices were pitched to rise. We found a larger single family, bank-owned home between Park Hill and Stapleton and were able to close on it for $136,000. The rehab was more inclusive, but with Kevin’s skill and good taste he created a very desirable rental which drew a very happy tenant. More cash flow. Today, we closed on his third rental property, in the heart of Park Hill. The $107,000 purchase price gives you an idea of what the market has done over the past few years and why Kevin is a happily building wealth through real estate. With a low down-payment, a well-planned fix-up budget and great interest rate, Kevin will be putting a total of $1,000 a month in his pocket this summer from his three investment properties. When you add in the tax benefits and property appreciation that comes with buying now and holding a long-term investment, Kevin is coming out way ahead.

How do you get into the real estate investing game? One house at a time. Real estate investing, like the stock market, can be daunting for some, but the payoff is worth the learning curve. My client, Kevin, became a landlord in 2007 with the purchase of his first rental property, half of a duplex in the City Park neighborhood of Denver. With a $150,000 purchase price and some minor upgrades to suit his specifications, Kevin was able to create positive cash flow within a few months. Two years later, we looked for another property, scouring for a neighborhood where you could still find a bargain, yet prices were pitched to rise. We found a larger single family, bank-owned home between Park Hill and Stapleton and were able to close on it for $136,000. The rehab was more inclusive, but with Kevin’s skill and good taste he created a very desirable rental which drew a very happy tenant. More cash flow. Today, we closed on his third rental property, in the heart of Park Hill. The $107,000 purchase price gives you an idea of what the market has done over the past few years and why Kevin is a happily building wealth through real estate. With a low down-payment, a well-planned fix-up budget and great interest rate, Kevin will be putting a total of $1,000 a month in his pocket this summer from his three investment properties. When you add in the tax benefits and property appreciation that comes with buying now and holding a long-term investment, Kevin is coming out way ahead.

Buying rental property is a great way for creative people to build long-term, sustainable wealth. For Kevin, this is the perfect blend of creativity and commerce and we’ll be following his journey through the fix-up process. Do you think this might be a good path for you? Call, text or email me, I’d be glad to show you successful strategies for building wealth through real estate. Till then, THRIVE BABY!